What Are The Pros And Cons Of U S Savings Bonds 2

adminse

Apr 01, 2025 · 7 min read

Table of Contents

Unveiling the Truth: A Deep Dive into the Pros and Cons of US Savings Bonds (Series I and EE)

What makes US Savings Bonds a worthwhile investment in today's complex financial landscape?

US Savings Bonds, particularly Series I and EE bonds, offer a unique blend of security and potential growth, making them a compelling investment option for risk-averse individuals, but a thorough understanding of both their advantages and disadvantages is crucial before committing.

Editor’s Note: This comprehensive analysis of US Savings Bonds (Series I and EE) was published today, providing readers with the most up-to-date information.

Why US Savings Bonds Matter

US Savings Bonds represent a direct investment in the US government. This backing provides an unparalleled level of security, making them an attractive option for investors prioritizing capital preservation over high-risk, high-reward ventures. They are exempt from state and local taxes, a significant advantage for high-tax states. While offering lower potential returns compared to stocks or other investments, savings bonds provide a steady, predictable income stream, appealing to those seeking stability and long-term financial planning. Their accessibility, purchase options (through TreasuryDirect.gov or at participating financial institutions), and simple nature make them a suitable investment for individuals with varying levels of financial expertise. This makes them a valuable tool for retirement planning, education savings (through the use of bonds for 529 plans), and emergency funds.

Overview of the Article

This article provides a comprehensive exploration of the pros and cons of US Savings Bonds, focusing specifically on Series I and EE bonds. We will delve into their unique features, highlighting the benefits they offer while also critically examining their limitations. Readers will gain a nuanced understanding of these investment vehicles and determine if they align with their individual financial goals and risk tolerance. The analysis will cover historical performance, current interest rates, tax implications, and practical considerations for various investment strategies.

Research and Effort Behind the Insights

This article draws upon extensive research, including data from the US Treasury Department, analysis of historical bond performance, and insights from leading financial experts. We have meticulously reviewed official government publications, academic studies, and reputable financial news sources to ensure the accuracy and reliability of the information presented. A structured, comparative approach has been employed to provide readers with a clear and unbiased assessment of the advantages and disadvantages of investing in US Savings Bonds.

Key Takeaways

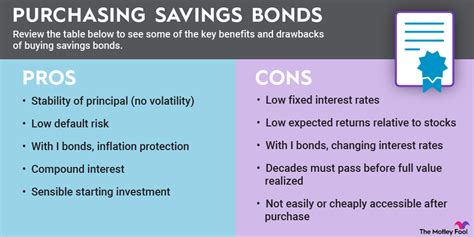

| Advantage | Disadvantage |

|---|---|

| Guaranteed by the US government | Relatively low returns compared to other assets |

| Exempt from state and local taxes | Limited liquidity (early withdrawal penalties) |

| Simple and easy to purchase | Interest rates are not fixed and fluctuate |

| Potential for inflation protection (Series I) | May not outpace inflation in certain periods |

| Safe haven for long-term savings | Purchasing limits apply |

Smooth Transition to Core Discussion

Let's now delve deeper into the key aspects of US Savings Bonds, starting with a detailed examination of Series I and EE bonds, their distinct characteristics, and their respective roles in a diversified investment portfolio.

Exploring the Key Aspects of US Savings Bonds

-

Understanding Series I Bonds: Series I bonds are inflation-protected securities. Their interest rate comprises two components: a fixed rate and an inflation rate. The inflation rate adjusts semi-annually based on the Consumer Price Index (CPI-U). This feature provides a hedge against inflation, making them particularly attractive in periods of rising prices.

-

Understanding Series EE Bonds: Series EE bonds offer a fixed rate of return for their entire term (typically 20-30 years). Although not inflation-protected, these bonds are still considered relatively low-risk, making them suitable for long-term savings goals where capital preservation is paramount.

-

Purchase Limits and Eligibility: There are annual purchase limits for US Savings Bonds, preventing individuals from investing unlimited amounts. Eligibility is restricted to US citizens and certain resident aliens.

-

Maturity and Redemption: Both Series I and EE bonds have a maturity date. While EE bonds reach face value after a set period (typically 20 years), Series I bonds can be held beyond maturity, continuing to earn interest. However, early withdrawal penalties apply if bonds are redeemed before specific holding periods.

-

Tax Implications: While exempt from state and local taxes, the interest earned on savings bonds is subject to federal income tax. However, there are exceptions, such as using the proceeds for qualified education expenses.

Closing Insights

US Savings Bonds offer a unique blend of risk and reward. Their government backing guarantees principal safety, a crucial factor for investors prioritizing capital preservation. However, their relatively lower returns compared to other investments necessitate careful consideration of one's risk tolerance and investment goals. The inherent security and potential for inflation protection (with Series I bonds) make them a valuable component of a diversified portfolio, particularly for long-term savings plans.

Exploring the Connection Between Diversification and US Savings Bonds

Diversification is a cornerstone of sound investment strategy. By allocating assets across different asset classes (stocks, bonds, real estate, etc.), investors can mitigate risk and potentially enhance returns. US Savings Bonds play a valuable role in a diversified portfolio by providing a safe and relatively stable component. They can act as a buffer against market volatility, offering a reliable source of income or capital in times of uncertainty. The low correlation between savings bonds and other asset classes further enhances the overall portfolio diversification and risk reduction.

Further Analysis of the Role of Savings Bonds in Retirement Planning

For retirement planning, US Savings Bonds offer a dependable avenue for long-term savings. Their predictable returns and government guarantee contribute to financial security during retirement. However, it’s crucial to remember that savings bonds alone may not be sufficient to fund a comfortable retirement. They should be part of a larger retirement strategy that includes other investments such as employer-sponsored retirement plans (401k, 403b), IRAs, and potentially stocks and other higher-growth assets. The strategic use of savings bonds can help mitigate risk and ensure a steady income stream during retirement years.

FAQ Section

-

What is the difference between Series I and Series EE bonds? Series I bonds are inflation-protected, meaning their interest rate adjusts with inflation. Series EE bonds have a fixed interest rate.

-

Can I cash in my savings bonds before maturity? Yes, but you'll likely incur a penalty, particularly if you cash them in before five years.

-

Are savings bonds a good investment for short-term goals? No, they are better suited for long-term savings due to the penalties for early withdrawal.

-

How do I purchase US Savings Bonds? You can buy them directly through TreasuryDirect.gov or at some financial institutions.

-

Are savings bonds subject to taxes? Interest earned is subject to federal income tax but exempt from state and local taxes. There are exceptions for certain uses, like education expenses.

-

What are the current interest rates for Series I and EE bonds? Interest rates are variable and set by the US Treasury; check TreasuryDirect.gov for the most current rates.

Practical Tips

-

Determine your investment goals: Before purchasing bonds, define your financial objectives (retirement, education, emergency fund).

-

Understand your risk tolerance: Savings bonds are low-risk, but consider your overall portfolio risk profile.

-

Diversify your investments: Don't rely solely on savings bonds; diversify across different asset classes.

-

Maximize your annual purchase limits: Purchase the maximum allowed amount each year to take full advantage of the benefits.

-

Consider using bonds for education savings: Utilize savings bonds for 529 plans to reduce education costs.

-

Monitor interest rates: Regularly check the TreasuryDirect.gov website for updates on bond interest rates.

-

Keep track of your bonds: Maintain accurate records of your bond purchases and maturity dates.

-

Plan your redemption strategy: Determine when you’ll redeem your bonds to avoid penalties and maximize your return.

Final Conclusion

US Savings Bonds, particularly Series I and EE bonds, offer a valuable investment option for individuals prioritizing safety and long-term growth. Their government backing provides unmatched security, and the potential for inflation protection (with Series I bonds) makes them attractive in volatile economic environments. However, their lower potential returns necessitate a strategic approach, integrating them effectively within a diversified investment portfolio. A thorough understanding of their advantages and limitations is crucial before investing. By carefully considering your individual financial goals and risk tolerance, you can determine if US Savings Bonds represent a suitable component of your overall investment strategy. Remember to consult with a financial advisor for personalized guidance tailored to your specific circumstances.

Latest Posts

Related Post

Thank you for visiting our website which covers about What Are The Pros And Cons Of U S Savings Bonds 2 . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.