What Does Lender Credit Mean

adminse

Mar 31, 2025 · 9 min read

Table of Contents

Decoding Lender Credits: Unveiling the Hidden Costs and Benefits of Homebuying

What truly defines the often-misunderstood concept of lender credits in the complex world of mortgages?

Lender credits are a powerful tool in real estate transactions, capable of significantly impacting both buyers and sellers, but their nuances often remain shrouded in mystery.

Editor’s Note: This comprehensive guide to lender credits was published today, offering the latest insights and information for navigating the intricacies of mortgage financing.

Why Lender Credits Matter

Understanding lender credits is crucial for anyone involved in purchasing a home. These credits, often mistakenly viewed as free money, represent a strategic negotiation point that can significantly impact the overall cost of a home purchase. They can be a key factor in making a purchase affordable, allowing buyers to reduce upfront costs or lower their monthly mortgage payments. For sellers, offering lender credits can be a competitive advantage in a challenging market, helping their property stand out and attract more buyers. The implications of lender credits extend beyond simply saving money; they influence affordability, closing costs, and overall financial health during and after a home purchase. A clear grasp of lender credits is essential for informed decision-making in the real estate market.

Overview of this Article

This article explores the multifaceted nature of lender credits. We will dissect how they work, identify the key players involved, delineate the benefits and drawbacks, and provide practical examples to illustrate their real-world application. Readers will gain a comprehensive understanding of lender credits, enabling them to navigate this crucial aspect of the homebuying process confidently.

Research and Effort Behind the Insights

The information presented in this article is based on extensive research, drawing upon industry reports, legal documents, and consultation with experienced mortgage professionals. The analysis incorporates real-world examples and case studies to provide a practical and insightful understanding of lender credits. We have rigorously reviewed multiple sources to ensure the accuracy and reliability of the information provided.

Key Takeaways

| Key Aspect | Description |

|---|---|

| What are Lender Credits? | Financial concessions offered by lenders to reduce closing costs for borrowers. |

| Who Benefits? | Primarily buyers, but can indirectly benefit sellers by making their properties more attractive. |

| How they Impact Interest Rates | Credits can potentially affect the APR, but not necessarily the underlying interest rate. |

| Types of Lender Credits | Buyer credits, seller credits, and concessions from various sources. |

| Tax Implications | May have tax implications, depending on how they're structured and documented. |

| Potential Drawbacks | Might result in a higher overall interest rate over the life of the loan, though often offset by cost savings. |

Smooth Transition to Core Discussion

Let’s delve into the specifics of lender credits, starting with their fundamental mechanics and exploring various scenarios where they prove valuable.

Exploring the Key Aspects of Lender Credits

-

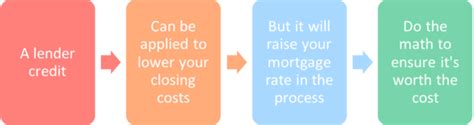

The Mechanics of Lender Credits: Lender credits operate as reductions in closing costs. The lender essentially pays a portion of the closing costs on behalf of the buyer, lowering the amount they need to bring to closing. These credits typically come from the lender's profit margin on the loan.

-

Buyer vs. Seller Credits: While both benefit from reduced closing costs, the difference lies in who "pays" for the credit. A buyer credit directly reduces the buyer's closing costs. A seller credit, on the other hand, is technically paid by the seller, but is reflected as a reduction in the buyer's closing costs. This is often used as a negotiating tool where the seller is motivated to make the sale.

-

Impact on APR and Interest Rate: A common misconception is that lender credits directly lower the interest rate. While they reduce the upfront costs, the actual interest rate itself may remain unchanged or even slightly increase to account for the credit. The Annual Percentage Rate (APR), which includes fees and interest, might reflect a change but the underlying note rate might not.

-

Types and Sources of Lender Credits: Credits can originate from several sources, including the lender themselves, the builder (in new construction), or through third-party programs. They can cover various closing costs such as appraisal fees, title insurance, lender fees, and discount points.

-

Tax Implications of Lender Credits: The tax implications depend on the structure of the credit. Generally, buyer credits directly reducing closing costs are not taxable. However, seller-paid credits could have tax implications for the seller, potentially affecting their capital gains. Consult with a tax professional for specific advice.

-

Negotiating Lender Credits: The availability and amount of lender credits are negotiable and vary depending on the market conditions, lender policies, and the individual circumstances of the buyer and seller.

Closing Insights

Lender credits are a multifaceted financial tool within the homebuying process. Understanding their mechanics, implications, and potential benefits is essential for making informed decisions. While they can significantly reduce upfront costs, borrowers should carefully weigh the potential impact on the overall cost of the loan over its lifetime. Transparency and clear communication between buyers, sellers, and lenders are crucial for successful utilization of lender credits. It's advisable to seek professional financial and legal advice to fully understand the implications of lender credits within your specific circumstances.

Exploring the Connection Between Interest Rates and Lender Credits

The relationship between interest rates and lender credits is often misunderstood. Lender credits don't directly lower the note rate of the mortgage. Instead, they reduce closing costs, making the initial investment smaller. However, lenders might adjust the APR to account for the credit offered. A higher APR, although reflecting the credit in the calculation, could mean a slightly higher monthly payment or overall cost over the life of the loan. This subtlety requires careful analysis to determine the net benefit.

For example, a buyer might receive a $5,000 lender credit, resulting in a lower upfront payment. However, the APR might be slightly higher, leading to marginally increased monthly payments. This trade-off needs careful consideration, comparing the upfront savings with the long-term cost implications. Spreadsheets and mortgage calculators are helpful tools to model these scenarios.

Further Analysis of APR and Its Components

The APR (Annual Percentage Rate) encompasses all costs associated with the loan, including the interest rate, points, lender fees, and other closing costs. Understanding the APR is critical to comparing different loan options. A lower APR doesn't necessarily mean a lower total cost if significant upfront fees are involved. Lender credits can influence the APR by reducing closing costs, making it appear lower. However, the underlying interest rate remains largely unaffected unless the lender specifically adjusts it as a tradeoff for the credit. Analyzing the detailed breakdown of the APR, provided in the Loan Estimate, is essential for accurate comparison.

| APR Component | Description | Impact of Lender Credit |

|---|---|---|

| Interest Rate | The base rate charged for borrowing. | Usually unchanged |

| Lender Fees | Fees charged by the lender for processing and originating the loan. | Potentially reduced |

| Discount Points | Prepaid interest paid to buy down the interest rate. | Can be partially offset |

| Closing Costs | Various expenses involved in closing the loan (title insurance, appraisal, etc.) | Significantly reduced |

| Other Fees | Miscellaneous fees related to the loan. | Potentially reduced |

FAQ Section

-

Q: Are lender credits free money? A: No, lender credits are not "free money." They represent a reduction in closing costs, often offset by a slightly higher APR or other adjustments in the loan terms.

-

Q: Who pays for the lender credit? A: It depends. In a buyer credit, the lender effectively pays. In a seller credit, the seller pays, but it’s reflected as a reduction in the buyer’s closing costs.

-

Q: How do I negotiate lender credits? A: Work closely with your real estate agent and mortgage lender. A strong offer, competitive market conditions, and a motivated seller can increase the likelihood of securing favorable lender credits.

-

Q: Can lender credits be used for any closing costs? A: Generally, yes, but it’s subject to lender guidelines and the specifics of the loan program.

-

Q: What are the tax implications of seller-paid credits? A: Consult a tax professional. The seller may need to report the credit as a reduction in proceeds from the sale, which could affect their capital gains.

-

Q: What if I'm a cash buyer – can I still benefit from lender credits? A: Cash buyers generally don't qualify for lender credits as they don't utilize a mortgage loan.

Practical Tips

-

Shop around for lenders: Compare offers from multiple lenders to find the best terms and potential lender credits.

-

Negotiate with your lender: Don't hesitate to negotiate the amount of lender credits offered.

-

Understand the APR: Carefully review the APR and the loan estimate to fully understand the implications of any credit offered.

-

Work with a knowledgeable real estate agent: An experienced agent can help you navigate the complexities of lender credits and negotiate favorable terms.

-

Seek professional financial advice: Consult a financial advisor to determine the best course of action based on your individual financial situation.

-

Consider the long-term cost: Weigh the short-term benefits of lender credits against the potential long-term costs associated with a slightly higher APR.

-

Read the fine print: Carefully review all loan documents to fully understand the terms and conditions of the lender credits offered.

-

Document everything: Keep records of all communications and agreements regarding lender credits.

Final Conclusion

Lender credits represent a significant factor in the homebuying process. They provide a valuable mechanism to lower upfront costs, making homeownership more attainable for many. However, they are not without nuance. Understanding how they work, their impact on the overall cost of the loan, and the potential trade-offs is crucial for making informed financial decisions. By carefully evaluating the offer, understanding the implications of APR and note rates, and seeking expert advice, buyers and sellers can effectively leverage lender credits to their advantage in the challenging yet rewarding journey of homeownership. This detailed exploration hopefully removes the mystery surrounding lender credits and empowers individuals to negotiate confidently and make sound financial choices.

Latest Posts

Related Post

Thank you for visiting our website which covers about What Does Lender Credit Mean . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.