What Factors Impact The Cost Of Your Life Insurance Premium

adminse

Mar 28, 2025 · 8 min read

Table of Contents

What Factors Impact the Cost of Your Life Insurance Premium? Unlocking the Secrets to Affordable Coverage

What determines the price you pay for life insurance, and how can you get the best value?

Understanding the factors that influence life insurance premiums is crucial for securing affordable and appropriate coverage.

Editor’s Note: This article on factors impacting life insurance premiums was published today.

Why Life Insurance Premiums Matter

Life insurance is a critical financial tool, providing a safety net for your loved ones in the event of your untimely death. However, the cost of this protection varies significantly, and understanding the contributing factors is paramount. Knowing what impacts premium costs empowers you to make informed decisions, secure the right coverage, and optimize your budget. The cost of life insurance isn't just a number; it directly affects your financial planning, influencing your ability to secure adequate coverage without straining your finances. This knowledge allows for better comparison shopping and negotiation with insurers, ultimately leading to a more financially sound decision.

Overview of this Article

This article delves into the multifaceted nature of life insurance premium calculations. We’ll explore the key factors influencing costs, ranging from personal demographics and health to policy type and coverage amount. Readers will gain actionable insights to help them navigate the life insurance market effectively and secure the best possible value for their needs. This will include a look at how different insurers assess risk, allowing for a more sophisticated understanding of the pricing process.

Research and Effort Behind the Insights

The insights presented in this article are based on extensive research, including analysis of industry reports from organizations like the American Council of Life Insurers (ACLI), data from leading insurance comparison websites, and consultations with experienced life insurance professionals. The information provided is intended to be informative and should not be considered financial advice. Always consult with a qualified financial advisor before making any significant financial decisions.

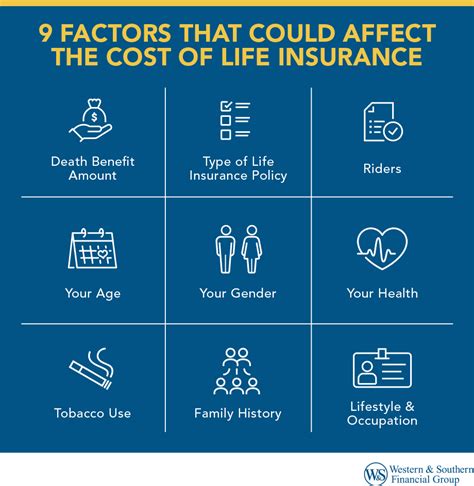

Key Factors Influencing Life Insurance Premiums

| Factor | Description | Impact on Premium |

|---|---|---|

| Age | Older applicants generally face higher premiums due to increased mortality risk. | Higher age = Higher premium |

| Health | Pre-existing conditions, current health status, lifestyle choices (smoking, diet, exercise) significantly impact premium costs. | Poor health = Higher premium |

| Gender | Traditionally, women have paid lower premiums than men, though this is changing due to increased longevity and regulatory changes. | Varies by insurer and gender-specific risk assessment |

| Lifestyle | Engaging in risky activities (e.g., extreme sports) or having hazardous occupations can lead to higher premiums. | Risky lifestyle = Higher premium |

| Policy Type | Term life insurance (temporary coverage) is generally cheaper than permanent life insurance (lifetime coverage). | Term life = Lower premium; Permanent life = Higher premium |

| Coverage Amount | Higher death benefit amounts result in higher premiums. | Higher coverage = Higher premium |

| Payment Frequency | Paying premiums annually usually results in lower overall costs than monthly or quarterly payments. | Annual payments = Lower premium |

| Insurer | Different insurers utilize different underwriting guidelines and pricing models, leading to variations in premiums for the same coverage. | Varies widely across insurers |

| Beneficiary Information | While less impactful than other factors, information about beneficiaries might be considered in some risk assessments. | Generally minimal impact |

| Occupation | Certain occupations are considered higher risk (e.g., firefighters, police officers) and may result in higher premiums. | High-risk occupations = Higher premium |

Let's dive deeper into the key aspects of life insurance premium determination, beginning with the most significant influences.

1. Age: The single most powerful predictor of life insurance costs is age. As you age, your risk of mortality increases, leading insurers to charge higher premiums to compensate for this increased risk. The younger you are when you purchase a policy, the lower your premiums will generally be. This is because you're statistically less likely to die in the near future compared to older applicants.

2. Health: Your health status is another crucial factor. Insurers carefully scrutinize your medical history, conducting thorough assessments to identify potential risk factors. Pre-existing conditions such as diabetes, heart disease, or cancer will significantly increase your premiums, as will current health concerns. Lifestyle choices such as smoking, excessive alcohol consumption, and a lack of physical activity also negatively impact your insurability and cost. Insurers may require medical exams or blood tests to assess your risk more accurately.

3. Lifestyle and Occupation: Engaging in high-risk activities like skydiving or mountain climbing can lead to higher premiums. Similarly, dangerous occupations such as construction work, mining, or firefighting often result in increased premiums due to the inherently higher risk of mortality or serious injury. The insurer needs to factor in the probability of early death caused by these activities.

4. Policy Type and Coverage Amount: The type of life insurance policy significantly impacts costs. Term life insurance provides coverage for a specific period (e.g., 10, 20, 30 years), offering a lower premium but no lifetime coverage. Permanent life insurance, such as whole life or universal life, offers lifetime coverage but comes with significantly higher premiums. The amount of coverage you choose also affects costs – a larger death benefit naturally leads to a higher premium.

5. Insurer Differences: Different insurance companies employ different underwriting processes and risk assessment models. Therefore, premiums for the same coverage can vary substantially between insurers. It's crucial to compare quotes from multiple companies to find the most competitive rates. Factors like the insurer's financial stability and claims-paying history should also be taken into consideration.

Exploring the Connection Between Health and Life Insurance Premiums

A person's health significantly impacts their life insurance premium. This isn't just about pre-existing conditions; it encompasses a holistic view of lifestyle and health choices.

-

Roles and Real-World Examples: Individuals with a history of heart disease, cancer, or diabetes will face higher premiums because these conditions increase the risk of premature death. A smoker will pay more than a non-smoker, reflecting the increased mortality risk associated with smoking.

-

Risks and Mitigations: Insurers mitigate these risks by applying higher premiums or even refusing coverage in extreme cases. Applicants can mitigate their risks by improving their lifestyle choices, getting regular check-ups, and actively managing pre-existing conditions.

-

Impact and Implications: Higher premiums for individuals with poor health can limit their ability to secure adequate coverage or force them to accept smaller death benefits. This can have serious financial consequences for their families.

Further Analysis of Health and Lifestyle Factors

The following table outlines the impact of specific health and lifestyle factors on life insurance premiums:

| Factor | Impact on Premium | Explanation |

|---|---|---|

| Smoking | Significantly higher | Increased risk of lung cancer, heart disease, and other health problems. |

| Obesity | Higher | Increased risk of diabetes, heart disease, and other health problems. |

| High Blood Pressure | Higher | Increased risk of stroke, heart attack, and kidney failure. |

| Diabetes | Significantly higher | Increased risk of heart disease, stroke, and other complications. |

| Cancer History | Significantly higher | Higher risk of recurrence and related health issues. |

FAQ Section

Q1: How often are life insurance premiums reviewed? A: Premium amounts are generally fixed for the duration of a term life insurance policy. For permanent life insurance, premiums may be adjusted as stipulated in the policy contract, but usually not frequently.

Q2: Can I lower my premiums after I purchase a policy? A: Once a policy is in effect, it's typically difficult to reduce premiums. However, some insurers may offer discounts for things like bundling insurance products.

Q3: What if my health improves after I purchase a policy? A: Most policies don't allow for premium adjustments based on improved health after the policy is issued.

Q4: Do all life insurance companies use the same underwriting criteria? A: No, underwriting criteria vary between companies. Some might be more lenient than others depending on their risk tolerance and pricing models.

Q5: What is the difference between term and whole life insurance? A: Term life insurance provides coverage for a set period, while whole life insurance offers lifetime coverage. Whole life premiums are higher, but it also builds cash value.

Q6: How much life insurance coverage do I need? A: This depends on individual circumstances, including income, dependents, debts, and desired legacy. Consult a financial advisor for personalized guidance.

Practical Tips for Securing Affordable Life Insurance

- Shop Around: Obtain quotes from multiple insurers to compare rates and coverage options.

- Improve Your Health: Making healthy lifestyle choices can significantly improve your insurability and lower premiums.

- Consider Term Life Insurance: For budget-conscious individuals, term life insurance offers a cost-effective way to secure temporary coverage.

- Pay Annually: Annual premium payments are usually cheaper than more frequent payments.

- Explore Discounts: Some insurers offer discounts for non-smokers, those who bundle policies, or who maintain healthy lifestyles.

- Review Your Coverage Regularly: Your life insurance needs may change over time, making periodic reviews crucial to ensure adequate coverage.

- Consider Your Beneficiaries: Clearly defining your beneficiaries can streamline the claims process and ensure your loved ones receive the benefits smoothly.

- Understand Policy Exclusions: Be sure to thoroughly review your policy to understand any limitations or exclusions that could impact coverage.

Final Conclusion

Understanding the factors that influence life insurance premiums is crucial for securing appropriate and affordable coverage. From age and health to policy type and lifestyle, numerous elements contribute to the cost. By carefully considering these factors and employing the practical tips outlined in this article, individuals can make informed decisions, optimize their budget, and ensure the financial security of their loved ones. Remember, life insurance is a long-term commitment, so proactive planning and diligent research are essential for achieving the best possible outcome. Don’t hesitate to seek professional guidance from a qualified insurance agent or financial advisor to personalize your coverage strategy.

Latest Posts

Related Post

Thank you for visiting our website which covers about What Factors Impact The Cost Of Your Life Insurance Premium . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.