How Do You Calculate The Real Rate Of Return On An Investment

adminse

Apr 01, 2025 · 9 min read

Table of Contents

Unlocking the Truth: How to Calculate the Real Rate of Return on an Investment

What truly matters: the nominal return or the actual purchasing power your investment generates?

Understanding the real rate of return is crucial for making sound financial decisions, separating hype from reality, and achieving your investment goals.

Editor’s Note: Calculating the real rate of return on an investment has been updated today to reflect the latest methodologies and economic considerations.

Why the Real Rate of Return Matters

Investors often focus on the nominal rate of return – the percentage increase in the investment's value. However, this figure fails to account for inflation, a critical factor eroding purchasing power. Inflation diminishes the value of money over time; a 10% nominal return means little if inflation simultaneously eats away at 5% of that gain. The real rate of return, on the other hand, adjusts the nominal return for inflation, providing a clearer picture of the investment's true performance in terms of increased purchasing power. This distinction is paramount for long-term financial planning, comparing different investment options, and accurately assessing the success of investment strategies. Understanding the real rate of return allows for more informed decisions about portfolio allocation, risk management, and retirement planning. Ignoring inflation leads to inaccurate assessments of profitability and can significantly hamper long-term financial success.

Overview of the Article

This article provides a comprehensive guide to calculating the real rate of return, covering various methods, considerations, and practical applications. We'll explore different approaches to calculating the real rate of return, examining their strengths and weaknesses. Readers will gain the tools and understanding necessary to accurately assess the true performance of their investments and make more informed financial decisions. The article will also delve into the impact of taxes and other factors on the real rate of return.

Research and Effort Behind the Insights

The information presented in this article is based on extensive research, incorporating established financial principles, economic data from reputable sources like the Bureau of Labor Statistics (BLS) and the Federal Reserve, and insights from leading financial textbooks and academic publications. The calculations and examples provided are designed to be practical and easily replicable for readers.

Key Takeaways

| Key Concept | Description |

|---|---|

| Nominal Rate of Return | The percentage increase in an investment's value without adjusting for inflation. |

| Real Rate of Return | The percentage increase in an investment's value after adjusting for inflation, reflecting true purchasing power. |

| Inflation Rate | The rate at which the general level of prices for goods and services is rising. |

| Fisher Equation | An approximate formula for calculating the real rate of return. |

| Exact Real Rate of Return | A precise calculation of the real rate of return, accounting for compounding effects. |

Smooth Transition to Core Discussion

Now, let's delve into the specifics of calculating the real rate of return, beginning with an understanding of the fundamental components involved: the nominal return and the inflation rate.

Exploring the Key Aspects of Calculating the Real Rate of Return

-

Understanding Nominal Return: The nominal rate of return is the simple percentage change in an investment's value over a given period. For example, if an investment grows from $100 to $110 in a year, the nominal return is 10%.

-

Determining the Inflation Rate: The inflation rate represents the percentage increase in the general price level of goods and services in an economy over a period. This is typically measured using consumer price indices (CPI) or other price indexes. These indices track the changes in the prices of a basket of goods and services representative of a typical consumer's spending. The inflation rate is crucial because it directly affects the purchasing power of money.

-

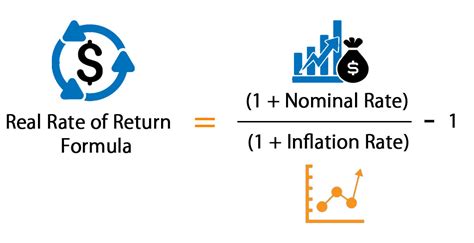

The Fisher Equation (Approximate Method): This is a widely used, albeit approximate, method for calculating the real rate of return. The formula is:

(1 + Nominal Rate) = (1 + Real Rate) * (1 + Inflation Rate)To solve for the real rate, rearrange the equation:

Real Rate ≈ (1 + Nominal Rate) / (1 + Inflation Rate) - 1This method is an approximation because it doesn't fully account for the compounding effect of inflation. However, it's useful for quick estimations, particularly when the inflation rate is relatively low.

-

Exact Real Rate of Return (Precise Method): For a more accurate calculation, especially over longer periods, consider the exact real rate of return. This method explicitly accounts for the compounding effect of both the investment growth and inflation. This is calculated as:

Real Rate = [(1 + Nominal Return) / (1 + Inflation Rate)] ^ (1/n) - 1Where 'n' is the number of periods (e.g., years). This formula offers a more precise representation of the true return, adjusted for the compounding effects of inflation.

-

Considering Taxes: The calculations above don't incorporate taxes. Capital gains taxes, especially, can significantly reduce the after-tax real rate of return. To account for taxes, you'd need to adjust the nominal return by subtracting the tax liability before applying the inflation adjustment.

-

Impact of Reinvestment: The frequency of reinvestment (e.g., dividends) affects the final real rate of return. More frequent reinvestments lead to compounding benefits, boosting the overall return, while less frequent reinvestments dampen this effect.

Closing Insights

Calculating the real rate of return is not merely an academic exercise; it's a critical skill for navigating the complexities of investing. By understanding and applying the methods discussed above, investors can gain a far more accurate picture of their investment performance, make informed decisions, and ultimately achieve their financial goals. The importance of factoring in inflation cannot be overstated, as it directly impacts the true purchasing power of your investment gains. Using both the approximate and exact methods provides a balanced approach, offering both speed and precision depending on the circumstances.

Exploring the Connection Between Risk and the Real Rate of Return

Risk is intrinsically linked to the real rate of return. Higher-risk investments, while potentially offering higher nominal returns, also often correlate with higher inflation sensitivity. This means that while the nominal return might be high, the real return could be significantly lower or even negative if inflation unexpectedly surges. For example, investing in emerging market equities might offer substantial nominal returns, but these are often accompanied by increased volatility and a higher correlation with inflation. Conversely, lower-risk investments like government bonds typically offer lower nominal returns but are less sensitive to inflation, often resulting in more stable real returns.

Further Analysis of Inflation's Impact

Inflation's impact extends beyond simply reducing the real rate of return. Unpredictable inflation creates uncertainty in the marketplace, making it more challenging to forecast future returns and affecting investment strategies. High and volatile inflation can also lead to distortions in the economy, disrupting market equilibrium and impacting business cycles. This makes understanding and accounting for inflation crucial for long-term investment planning. To illustrate this further, consider a scenario where an investment yields a 10% nominal return, but inflation is 12%. The real rate of return is negative (-1.8%), implying a loss in purchasing power despite the positive nominal return. This highlights the critical importance of adjusting for inflation.

FAQ Section

-

Q: What is the best method for calculating the real rate of return?

A: The "best" method depends on the context. The Fisher equation is suitable for quick estimations and low inflation rates. The exact method provides a more precise calculation, especially for longer periods or higher inflation rates.

-

Q: How often should I calculate my real rate of return?

A: Ideally, you should calculate your real rate of return annually or whenever you rebalance your portfolio. This allows for timely monitoring of performance and adjustments to your investment strategy.

-

Q: What if the inflation rate is negative (deflation)?

A: If the inflation rate is negative (deflation), the real rate of return will be higher than the nominal rate. This is because your money retains more purchasing power.

-

Q: Does the real rate of return account for taxes?

A: No, the standard real rate of return calculations do not inherently account for taxes. You must adjust the nominal return for taxes before applying the inflation adjustment for an accurate after-tax real rate of return.

-

Q: Where can I find reliable inflation data?

A: Reliable inflation data can be obtained from government sources like the Bureau of Labor Statistics (BLS) in the US, or equivalent statistical agencies in other countries.

-

Q: How does the real rate of return influence investment decisions?

A: The real rate of return provides a clearer picture of an investment's true performance, allowing for better comparisons between different investments and aiding in more informed investment decisions aligned with your risk tolerance and financial goals.

Practical Tips

-

Track your investments regularly: Maintain accurate records of all your investments and their returns.

-

Find reliable inflation data: Use data from reputable sources like the BLS to accurately calculate the real rate of return.

-

Use appropriate calculation methods: Employ the Fisher equation for quick estimations and the exact method for greater accuracy, especially over longer periods.

-

Consider taxes: Adjust your nominal return for taxes before calculating the real rate of return for a complete picture.

-

Rebalance your portfolio regularly: Periodically rebalance your portfolio to maintain your desired asset allocation and risk level.

-

Consult a financial advisor: If needed, seek professional financial advice to help you understand and manage your investments effectively.

-

Understand your risk tolerance: Align your investment choices with your risk tolerance and financial goals.

-

Consider diversifying your investments: Diversification can help mitigate risk and improve your overall real rate of return over the long term.

Final Conclusion

Accurately calculating the real rate of return is an essential skill for any investor. It allows you to cut through the noise of nominal returns and see the true impact of your investments on your purchasing power. By understanding the methods outlined in this article, and by consistently tracking your investments and considering the influence of inflation and taxes, you can gain a far clearer understanding of your investment success and make more informed decisions to achieve your long-term financial goals. The quest for financial success is not simply about accumulating wealth; it's about maximizing the real, inflation-adjusted value of that wealth. Mastering the calculation of the real rate of return is a significant step towards that goal.

Latest Posts

Related Post

Thank you for visiting our website which covers about How Do You Calculate The Real Rate Of Return On An Investment . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.